This article reflects my opinion and some back of the envelope calculations on the emerging digital medical education market in India.

Current Scenario

The data

Here are the potential market opportunities that exist for digital first platforms - Marrow and Unacademy:

- Total number of medical seats in KA: 9345

- Meaning that each academic batch has 9345 students. Total students would be around 5 years of medicine x 9345 -> 46,725 students

- Total number of medical colleges: 58

- Number of medical seats per college - average: 161 seats

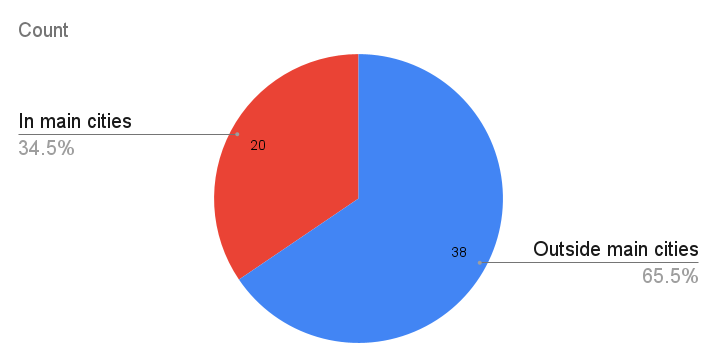

- Colleges located in the main cities - Bangalore and Mangalore -> 21

- Colleges located outside the main cities -> 38

Aggregation of colleges:

- Total colleges: 59

- 20 medical colleges are in two main cities - Bangalore and Mangalore. This is where the offline first players such as DAMS and Dr.Bhatia serve.

- 38 medical colleges are outside these big cities and are scattered all over KA. These cannot be served effectively by these offline players (They do have online satellite classes that are conducted every weekend)

- The 38 medical colleges have 6,118 students in them.

How much are these students willing to spend:

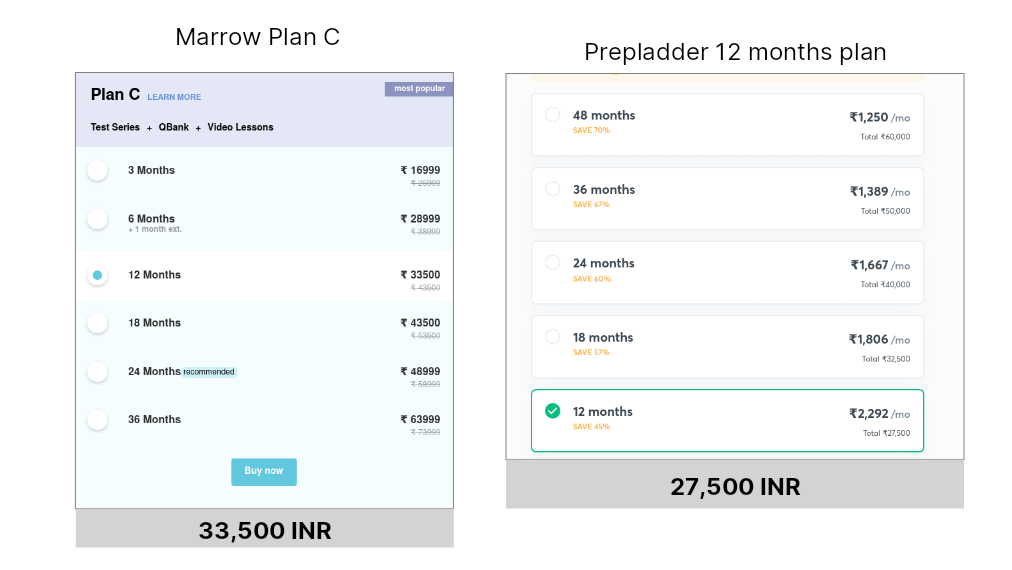

Taking the current market pricing of Marrow and Unacademy for the 12 month plan:

Now the assumptions

None of these companies post their cash flows online, so I have to make a few assumptions regarding their adoption:

- Potential market: 38 college x 161 students -> 6,118

- Adoption rate of 30%: From what I've asked around it is 30% because their courses are priced on the higher end.

- Students that probably own a plan(in 1 year academic batch): 1835

- Median price estimate (Marrow + Unacademy): 30,500 INR

- Total capture: 5.60 Cr or 55 million INR or $700,00

Things I have missed out: [1] Students in main cities also buy these plans [2] These platforms often offer discounts ranging from 20% to 50%. [3] Students often also split costs and share the platform accounts

Risks

Above is a rough graph on the ever growing digital medical education space

The space is now teeming more than ever with competitors. Now Marrow and Prepladder are not the only ones in the space. The established offline players have also gone online since the COVID lockdown. Main ones are:

- eMedicoz by Delhi Academy of Medical Sciences - a major offline coaching player

- e-Gurukul by Dr. Bhatia Medical Coaching Institute

Above is the package offered by Dr.Bhatias e-gurukul - 16,112 INR

Above is the package offered by Dr.Bhatias e-gurukul - 16,112 INR

The offline players have some serious advantages as they are more experienced institutions:

- Teachers that have experience

- Already existing repute

- Already existing video bank The above factors only mean one thing - cheaper pricing point

Dr. Bhatia's e-gurukul is 50% cheaper than Marrow

| Brand | Cost for video only plan (INR) | Link |

|---|---|---|

| Marrow | 33,500 | https://www.marrow.com/pro |

| Unacademy | 27,500 | https://unacademy.com/goal/neet-pg/SDDOC/subscribe |

| e-Gurukul (from Dr.Bhatia) | 16,000 | https://www.egurukulapp.com/package/plan/NEET-PG-Program |

| eMedicoz (from DAMS) | 30,000 | https://emedicoz.com/web/Courses/live_course_detail?id=642&title=DAMS%20Master%20Plan |

| A price band comparison of all the top brands |

Advantages

1.VC money

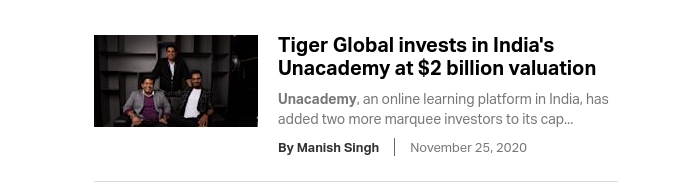

Above is an example of venture capitalist investment into unacademy

Venture capitalists are big investment groups that invest money into startups. Think Zuckerburgs Facebook ventures or Reid Hoffmans Greylock ventures

Unacademy acquired prepladder sometime last year, read here in a report by Techcrunch for $50 million. This is exactly abnormal in the startup ecospace but is very surprising considering that Prepladder catered to medical student coaching exclusively online. This means that Unacademy now has courses all the way from National Eligibility Entrance Test for Undergraduates to Postgraduate entrance exam to USMLE.

Marrow also has the same story, Japan's M3 group acquired its parent company Neuroglia health for an undisclosed amount, read the story here. Marrow specializes exclusively in the MBBS education content and owns an app called Dailyrounds that caters to 450,000 doctors.

VC money is key for a few reasons:

- VC's bring market expertise with them. Japans M3 specializes in healthcare field only

- These companies can venture into new areas and spend more time on outreach and marketing

- Most VC's are usually headed by technology experts - which means they deliver an expertise in technology as well

2.Software is complex

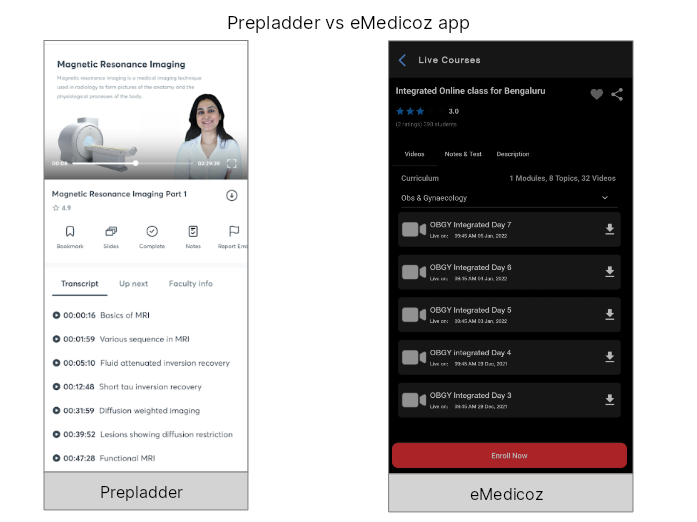

Expertise in technology and healthcare seem to be mutually exclusive in this STEM education obsessed Indian education ecosystem. So when offline players such as DAMS tried to get into the virtual club they faced a lot of problems related to execution. This is in contrast to Marrow and Prepladder who have in house technical expertise related to execution.

Above image is that stark contrast between the apps of Prepladder(Now Unacademy) and eMedicoz(by DAMS). Though they deliver nearly the same content, the User Experience is significantly is better on Prepladder.

3.Marketing

VC Money brings an expertise in marketing as well, targeting niche groups of students who are most likely to buy their plans. Here's basics of the approach:

- College quiz and academic programs are often underfunded(Like the one above)

- Marrow or Prepladder swoop in and ask to sponsor the programs

- In exchange the program directors provide Marrow or Prepladder with data of participant students

- The students who win the contest now get a sponsored content plan

- The firms get a vetted list of students who are participating in academia and hence are the ones most likely to buy their plans

Conclusion

The digital medical education space seems to be heating with acquisitions to mergers to evolving approaches. The gap between digital first players (Marrow and Prepladder) and offline integrated players (DAMS and DBMCI) is reducing fast. All in all, this field is heating up and worth watching.